AUBURN, Ala., April 17, 2026 – Federal Reserve Governor Christopher Waller said the central bank could still lower interest rates later this year, but cautioned that persistent energy market disruptions linked to tensions around Iran risk keeping inflation elevated and complicating the policy outlook.

Speaking at Auburn University, Waller described the current environment as one shaped by repeated supply shocks, with the latest centered on oil flows through the Strait of Hormuz, a critical chokepoint for global energy trade.

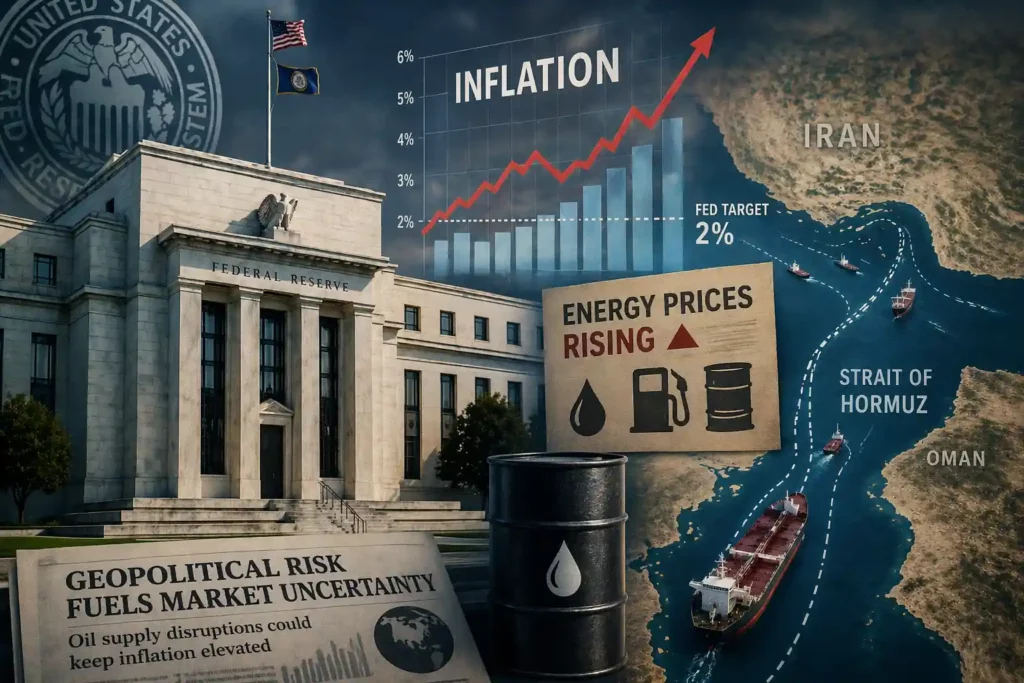

Strait of Hormuz risk and global oil exposure

Roughly one fifth of the world’s oil consumption passes through the Strait of Hormuz, making it one of the most strategically sensitive corridors in the global economy. Even partial disruptions tend to push crude prices sharply higher in the short term.

For the United States, the direct dependence on Gulf oil has declined over the past decade due to increased domestic production. However, U.S. inflation remains exposed to global oil benchmarks, since petroleum products are priced on integrated international markets.

Waller’s concern is not the initial spike, but its duration. Short lived increases in oil prices have historically had limited and reversible effects on inflation. Prolonged shocks, by contrast, can feed into transportation costs, industrial inputs, and eventually consumer prices more broadly.

Inflation dynamics and the Fed’s preferred gauge

The Personal Consumption Expenditures Price Index remains central to the Fed’s assessment. As of early 2026, headline PCE inflation has been running above the 2 percent target, with energy contributing to renewed upward pressure.

Core PCE, which excludes food and energy, is typically more stable. However, Waller noted that extended periods of high energy costs can bleed into core measures over time, particularly through services such as logistics, air travel, and housing related costs.

This distinction is critical for policy. If inflation pressures remain confined to volatile components, the Fed can afford to be patient. If they broaden, the case for holding rates higher strengthens.

Historical precedent shapes current caution

Waller’s framework echoes past episodes where energy shocks complicated monetary policy.

During the 1970s oil crises, supply disruptions led to sustained inflation that became embedded in expectations, forcing aggressive tightening later on. More recently, the 2021–2022 post-pandemic energy surge contributed to the sharpest inflation spike in decades, prompting the Fed’s fastest rate hiking cycle since the 1980s.

The lesson policymakers draw is clear. Acting too quickly to ease policy in the face of persistent supply driven inflation risks reigniting broader price instability.

Two policy paths remain in play

Waller outlined a conditional outlook rather than a fixed trajectory.

If energy markets stabilize and oil prices retreat, inflation could resume its gradual decline. In that scenario, the Federal Reserve would have room to begin lowering rates, particularly if labor market conditions soften.

If disruptions persist, however, inflation could remain above target for longer. That would likely delay any easing cycle and keep borrowing costs elevated, even as growth slows.

The key variable is not the geopolitical event itself, but its economic transmission, especially how long elevated energy prices last and how broadly they spread through the economy.

Market implications and policy signaling

Financial markets have been highly sensitive to shifts in rate expectations. Earlier in the year, investors anticipated multiple rate cuts in 2026. Waller’s remarks reinforce a more cautious view.

His emphasis on data dependency signals that the Fed is not committing to a timeline. Instead, policymakers are watching a combination of inflation readings, energy prices, and broader economic indicators before making any move.

This approach reflects a broader shift in central banking communication. Rather than forward guidance tied to dates, the Fed is increasingly framing decisions around evolving conditions.

Outlook

Waller’s April 17 speech underscores the growing influence of global supply shocks on U.S. monetary policy.

Rate cuts remain possible in 2026, but they are contingent on inflation moving convincingly toward target. As long as energy markets remain volatile, that progress is uncertain.

For now, the Fed’s stance is one of cautious flexibility, balancing the risk of easing too soon against the cost of keeping policy tight for longer.